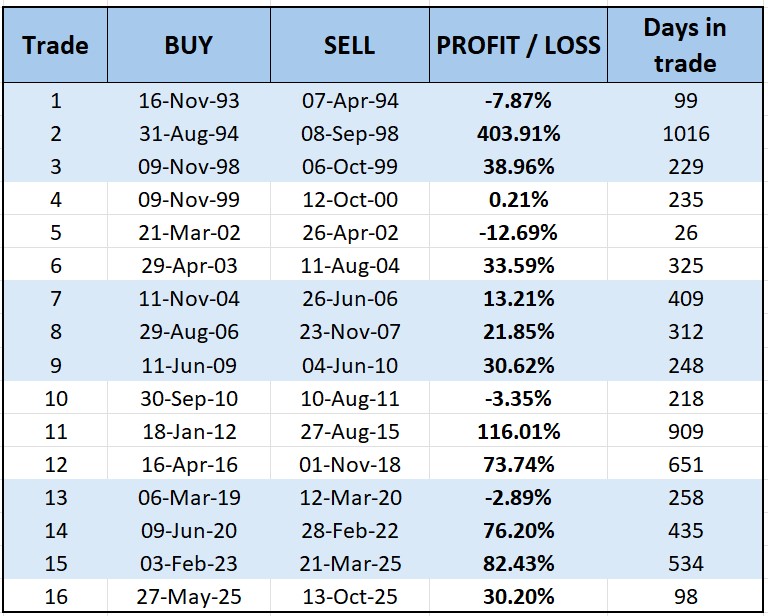

These are the exact trades generated by the ITM rules on SPY from 1993 – 2025.

Bull Market Results Summary - SPY

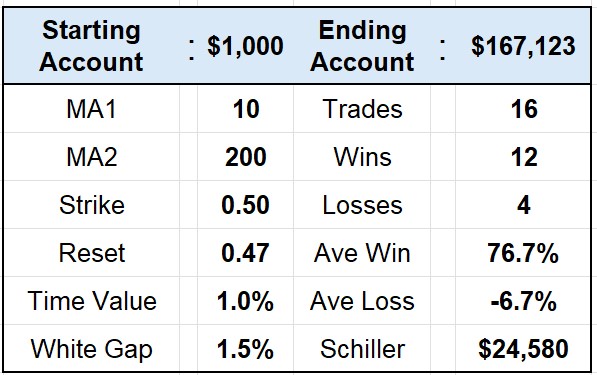

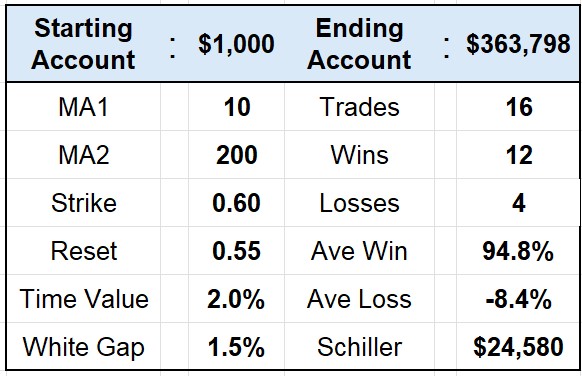

The SPY backtest covers multiple full market cycles and applies the same entry and exit rules throughout the test period.

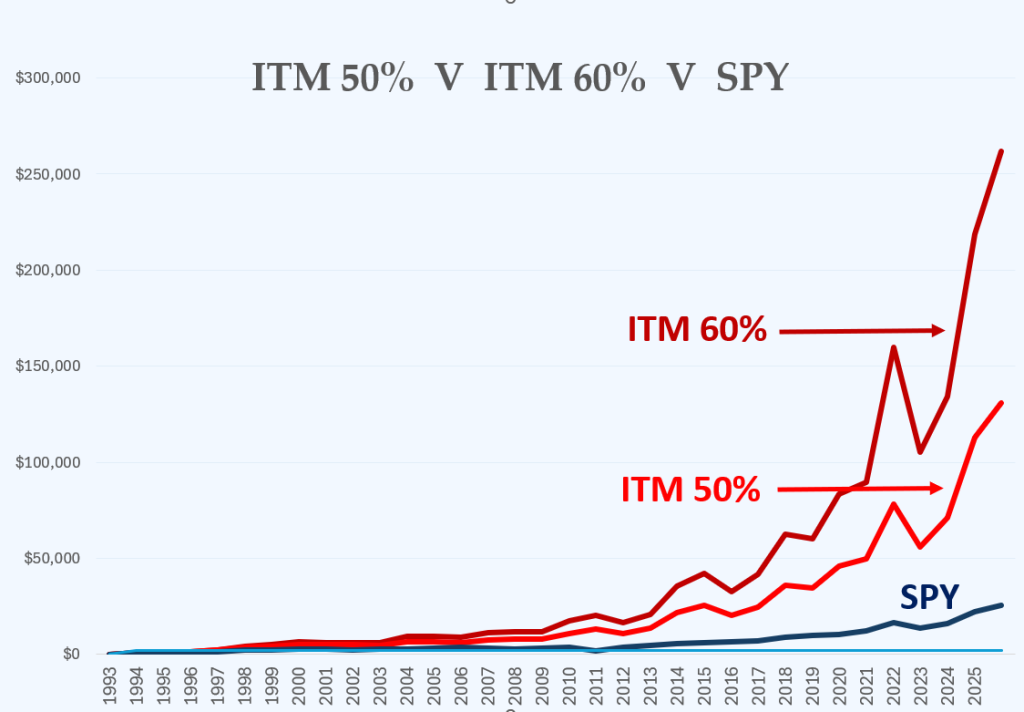

Results are shown for both the 50% and 60% in-the-money variants of the ITM strategy, allowing comparison of behaviour under identical market conditions.

Results Summary - SPY 50% Strike

Results Summary - SPY 60% Strike

Trade List - SPY

The following trade lists show all SPY positions generated by the ITM rules 1993 – 2025

NOTE: The trade dates shown are identical for both the 50% and 60% in-the-money variants of the ITM strategy; only the option strike selection differs.

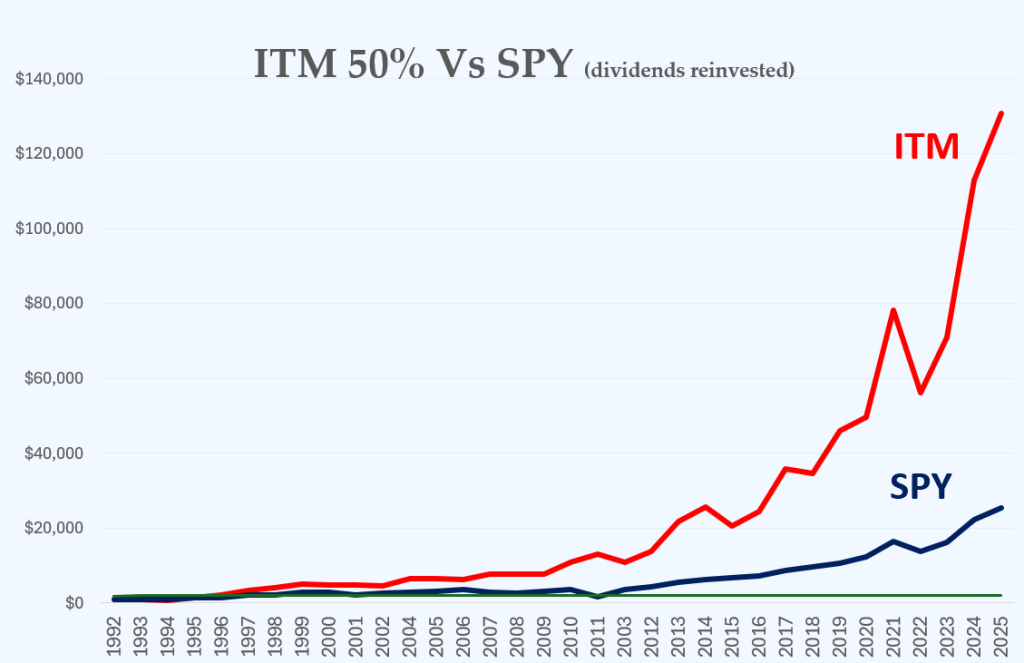

Performance Graphs - SPY

The graphs below show the cumulative performance of the ITM strategy applied to SPY 1993 – 2025

SPY Shares Performance 1993-2025

Comparison ITM 50% Strike Vs SPY

Comparison ITM 50% & ITM 60% Strikes Vs SPY

Summary Notes - SPY

All SPY results shown on this page are generated from the same underlying trade signals and timing. Differences between the 50% and 60% in-the-money variants arise from option structure rather than trade selection. Full methodology and assumptions are on the main Backtesting page.

Thank you – your message has been sent.

You will be notified when there is a new blog post.

Please note that Heather answers all questions at the end of the ITM Blog.

Happy trading!

We noticed you're visiting from United States (US). We've updated our prices to United States (US) dollar for your shopping convenience. Use Australian dollar instead.Dismiss