Bear markets behave very differently from bull markets. Bear markets were analysed individually rather than as a continuous period.

Capital was reset at the start of each bear market, as bull-market trades occurred between these periods..

Trade frequency varies significantly between bears, with some producing only a small number of qualifying trades.

Bear markets behave very differently from bull markets. Bear markets were analysed individually rather than as a continuous period. Capital was reset at the start of each bear market, as bull-market trades occurred between these periods.. Trade frequency varies significantly between bears, with some producing only a small number of qualifying trades.

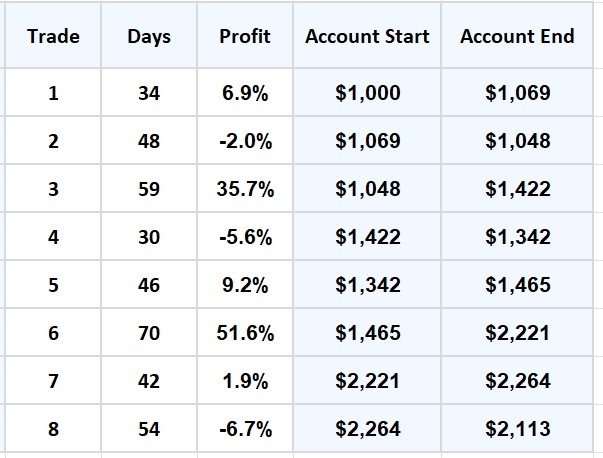

2000-2003 Bear Market (TechWreck)

This bear market produced 8 qualifying ITM trades.

The effect on the account balance

The 2000–2003 bear market was prolonged and volatile, with sharp counter-trend rallies occurring throughout the decline. Although the broader market fell heavily over this period, several ITM trades delivered substantial gains when these rallies emerged. As with all bear markets, trade frequency was low, but outcomes were driven by the size and timing of individual moves rather than by continuous exposure.

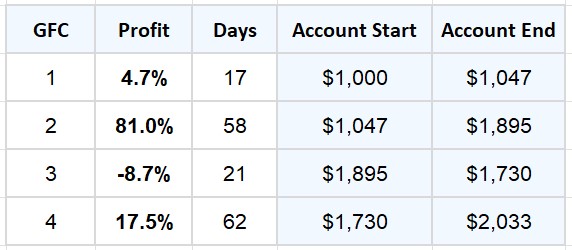

2007 - 2009 Bear Market (GFC)

This bear market produced 4 qualifying ITM trades.

The effect on the account balance

The Global Financial Crisis was characterised by extreme volatility and unusually large price swings. Although the number of qualifying ITM trades was small, several occurred during sharp counter-trend rallies, producing outsized gains over short timeframes. As with other bear markets, outcomes were driven by the magnitude of individual moves rather than by frequent trading.

2018

In late 2018 the market experienced a sharp but short-lived decline that is often described as an “almost bear.” During this period, ITM did not enter a trade, as the qualifying conditions were not met. The decline occurred over the Christmas and New Year period and reversed quickly, limiting both trade duration and opportunity.

2020 Bear Market (Covid)

This bear market produced only 1 qualifying ITM trade.

The effect on the account balance

Although short-lived, the COVID bear market produced a fast-moving counter-trend rally that resulted in a single qualifying ITM trade. As with other bear markets, outcomes were driven by the size and speed of the move rather than by trade frequency.

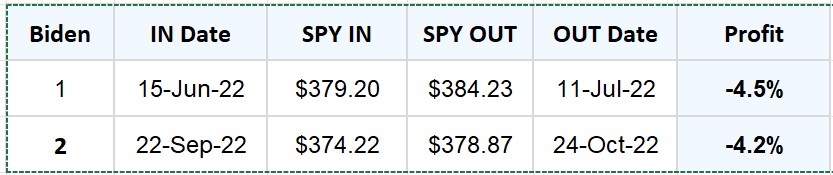

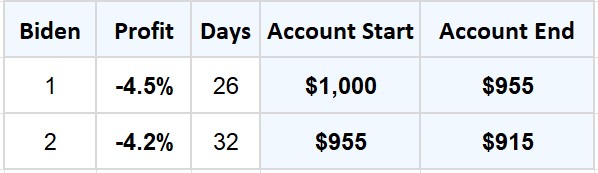

2022 Bear Market (Inflation)

This bear market produced 2 qualifying ITM trades.

The effect on the account balance

This bear market generated only two qualifying ITM trades, both of which resulted in small losses. As with other bear markets, the limited number of opportunities reflected the absence of sustained counter-trend rallies rather than a failure of the underlying rules.

Bear Market Trading Summary

Bear markets are irregular and highly variable, producing far fewer qualifying ITM trades than extended bull markets. For this reason, each bear market was analysed independently, with capital reset at the start of each period. Outcomes were driven by the size and timing of individual counter-trend rallies rather than by trade frequency. These results illustrate how ITM behaves during periods of market stress, complementing the longer-term bull-market backtesting shown earlier.

Thank you – your message has been sent.

You will be notified when there is a new blog post.

Please note that Heather answers all questions at the end of the ITM Blog.