Some of the most dangerous ideas in trading sound perfectly sensible. This chapter breaks down two of them – leveraged ETFs and protective puts – and shows why both can quietly erode your results.

Ch 19 Overview

Leverage & Protection

Ch 19 : Essentials in 14

Points

Leverage & Protection

Ch 19 : Podcast

Leverage & Protection

Ch 19 : Video

Leverage & Protection

Ch 19 : Glossary

Leverage & Protection

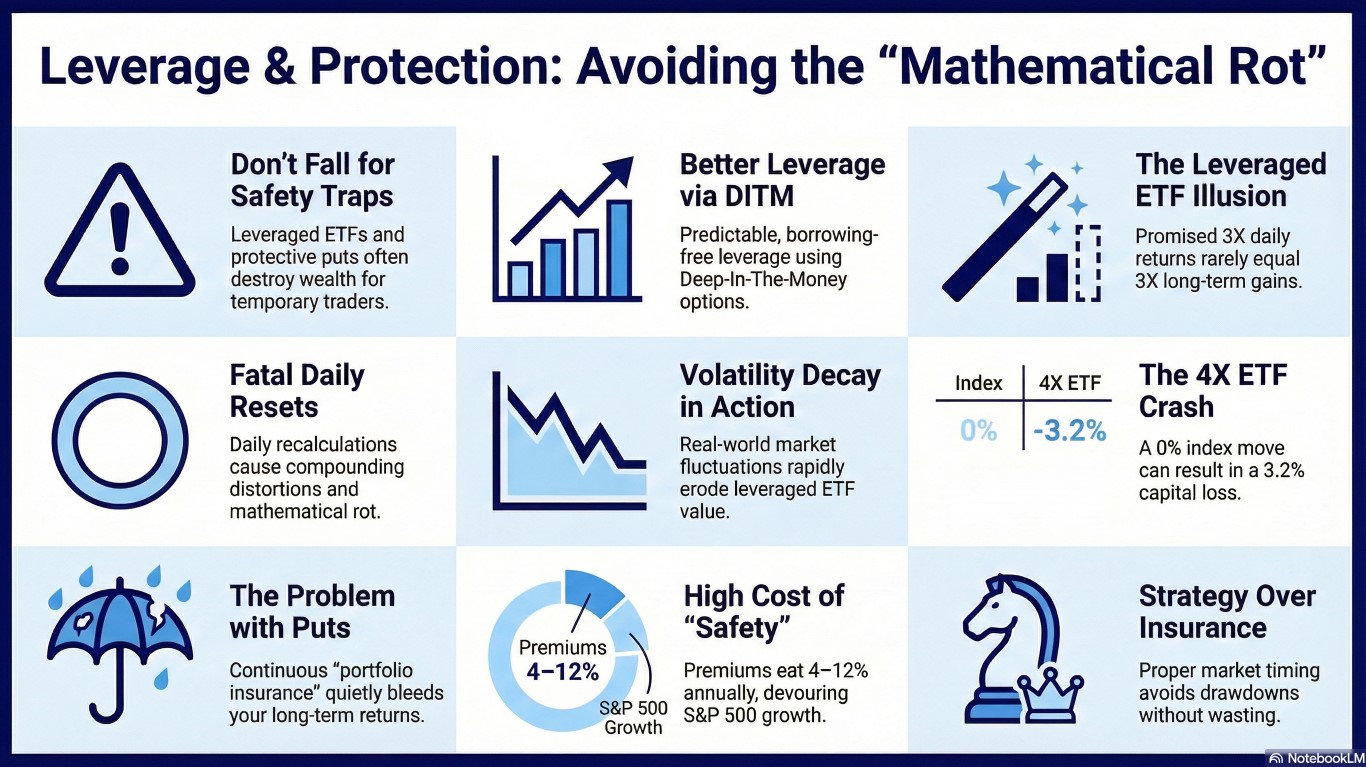

Chapter 19 is all about avoiding two massive traps that temporary traders love: leveraged ETFs and expensive portfolio insurance. Let’s cut to the chase and define the new concepts:

Daily Reset: The hidden trap built right into leveraged ETFs, where they recalculate and re-leverage themselves back to their target multiple every single day. This daily compounding is exactly what destroys their long-term performance.

Inverse Leveraged ETFs: The bearish versions of leveraged ETFs (like the -2X SDS or -3X SPXU) that promise to deliver a multiple of the market’s daily drop.

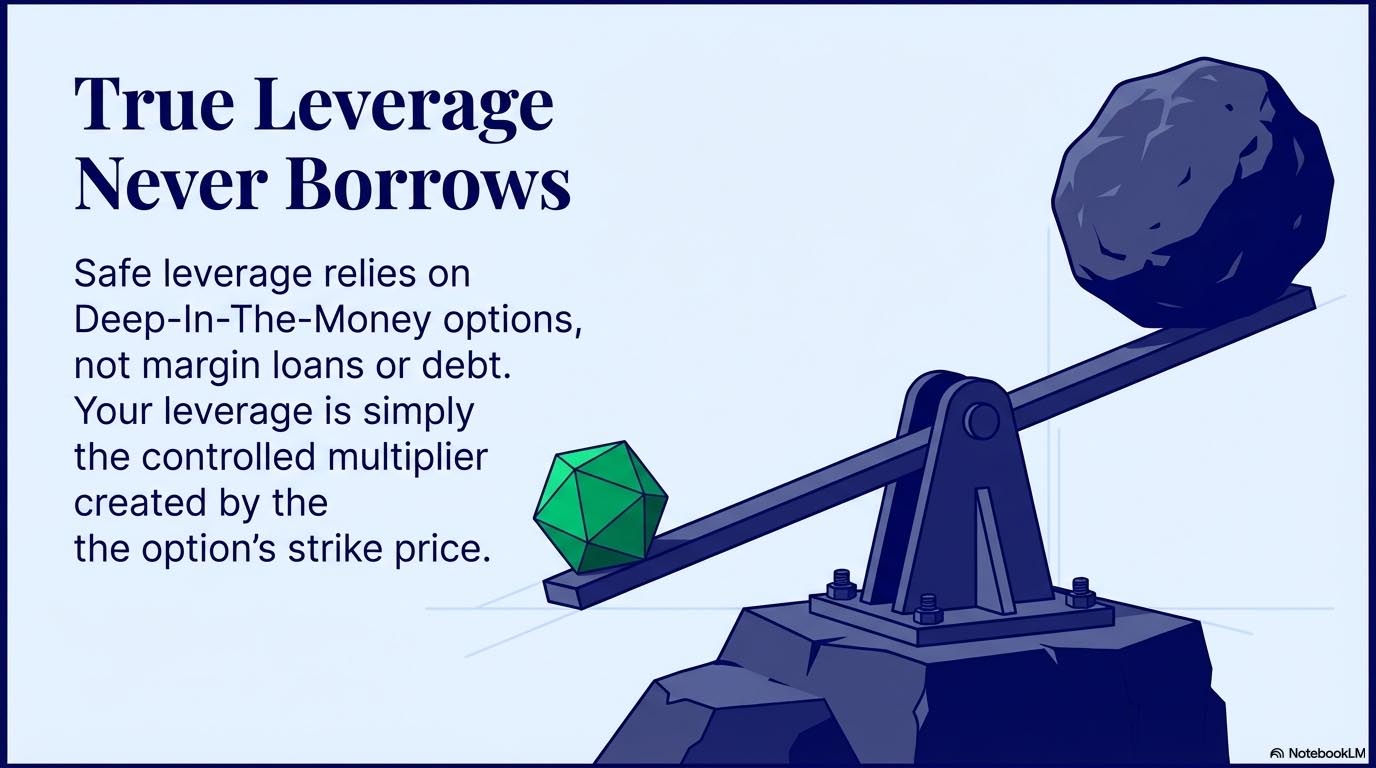

Leverage (ITM Style): Safe, predictable leverage achieved purely by buying Deep-In-The-Money (DITM) options. Unlike traditional margin, the ITM strategy never borrows a single cent to achieve its multiplier, so you can never lose more than you own.

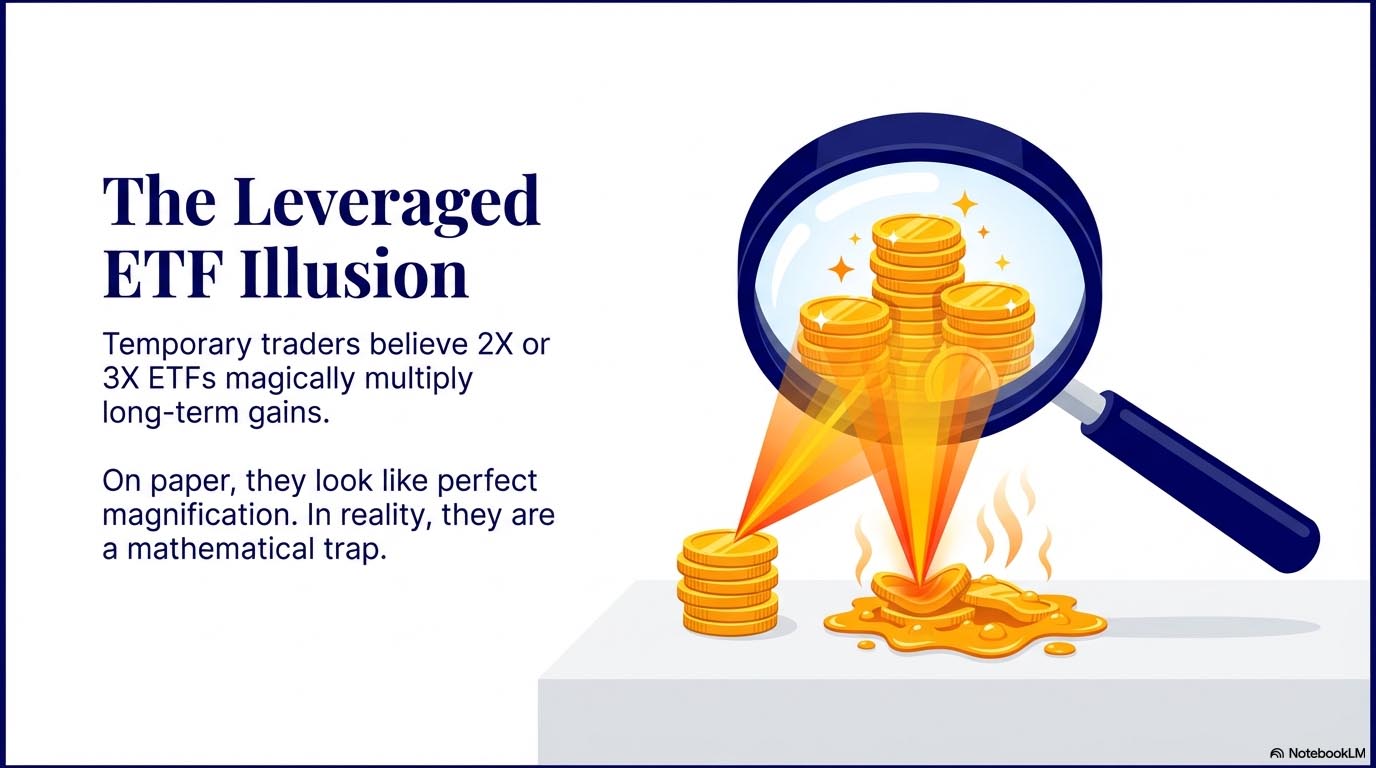

Leveraged ETFs: Highly dangerous funds that promise to deliver multiples (2X, 3X, 4X) of an index’s daily return. While they sound seductively simple for smaller accounts, their daily resets cause them to diverge wildly from the actual index over weeks or months, often wiping out the traders who buy them.

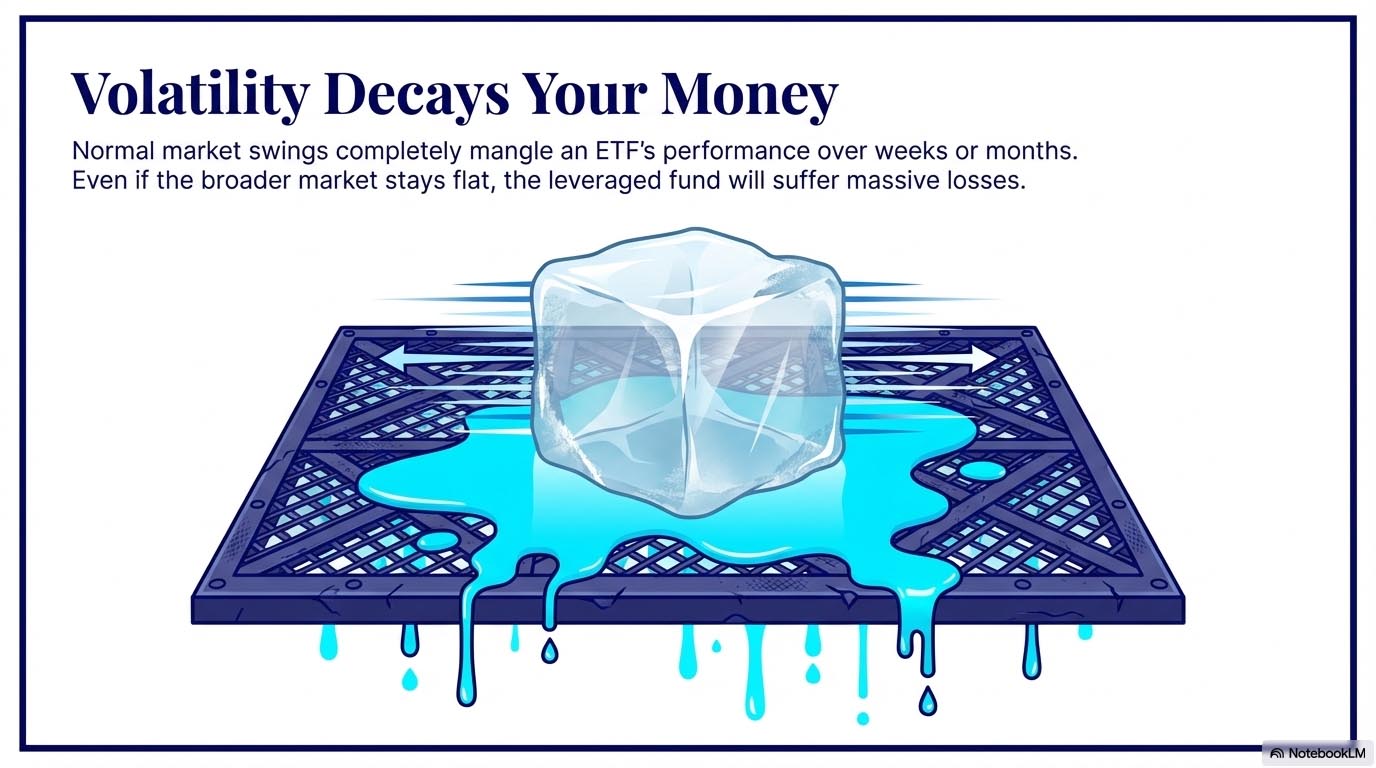

Mathematical Rot / Volatility Decay: The compounding distortions that eat away at a leveraged ETF’s value in any normal, fluctuating market. Because of the math behind daily resets, even if the underlying index drops and recovers to sit relatively flat over a few weeks, the leveraged ETF will still suffer significant losses.

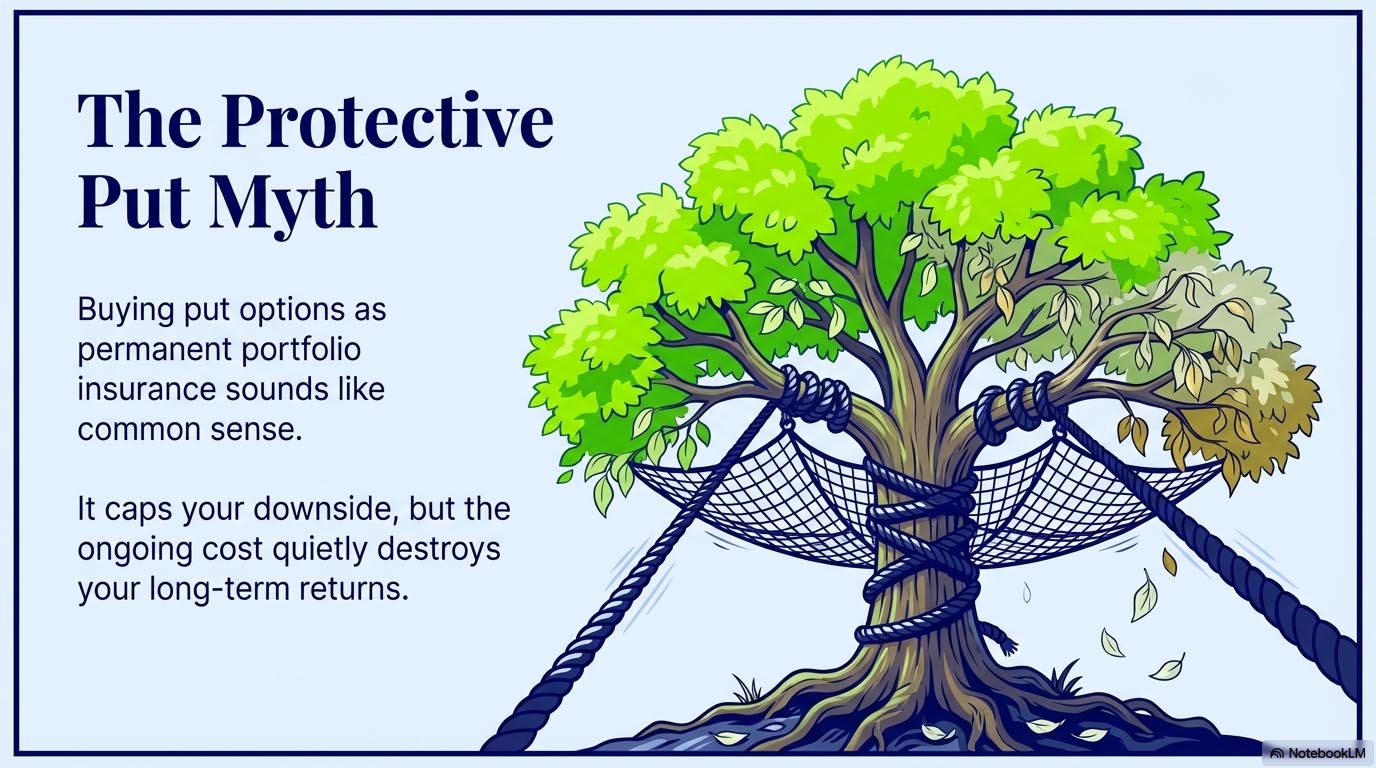

Premium Bleed: The quiet destruction of your long-term returns caused by constantly paying for portfolio insurance. Constantly buying protective puts can eat up 4% to 12% of your account per year, essentially handing over nearly all of your natural market growth to option premiums.

Protective Puts: Buying a put option below the current market price to act as an “insurance policy” on shares you already own, theoretically capping your maximum downside. The author strongly advises against them as an ongoing strategy because they are expensive, they usually expire worthless, and their prices explode exactly when you need them most. The ITM strategy avoids them entirely by simply exiting the market early when momentum turns.

Ready To Test Yourself?

Chapter 19 Quiz

Chapter 19 Quiz

Leverage & Protection

Loading...

Quiz Complete!

You scored /

Thank you – your message has been sent.

You will be notified when there is a new blog post.

Please note that Heather answers all questions at the end of the ITM Blog.