The Psychology of Boredom.

Since late October, SPY and QQQ have been going nowhere. Plenty of headlines. Plenty of “analysis.” but the reality is just motion without progress. Push to the top of the range. Fail. Drift lower. Hold. Push up again. Rinse. Repeat.

An expert on every corner

Sideways markets are where new “experts” are born. Nothing decisive is happening, every small move is explained with unwarranted certainty.

The longer the range persists, the more confident the predictions become. Every push toward the upper boundary is “the breakout.” Every dip is “the correction we’ve been waiting for.”

Clarity is decreasing, but the predictions are getting louder.

Buying the dip

‘Buying the dip’ and ‘momentum’ strategies that thrived in a bull market stall in a sideways market. Dips become brief bounces, momentum stalls at the top of the trading range, and the stillness breeds restlessness. Boredom. What worked well in an uptrend starts to feel wrong.

Humans need action

Humans are wired for action. When nothing decisive happens, the urge to intervene grows.

Systems get “adjusted.”

Positions get tweaked.

Strategies get doubted.

New strategies get tested. Because surely something must be done. Perhaps ‘this time it’s different’.

Bull markets excite

When the markets is going up, traders are happy, everyone wants to get in on the party.

There’s no need for action – the trend is giving you all the action you need.

Bear Markets Terrify

When there’s a dip the fear strikes the heart of the trader. Action feels justified.

They dump their positions.

They join the ‘I told you so’ crowd.

The press is filled with gloom and doom stories, confirming their decisions.

Consolidations Irritate

Sideways markets don’t create panic. They create restlessness. Boredom. There’s no crash to respond to. No rally to celebrate. Just months of motion without progress. And that’s psychologically difficult and creates a crisis of confidence that tempts traders to abandon their rules right when they are most needed.

This psychological fatigue leads to “fiddling” with entries or skipping valid signals, often resulting in the trader being sidelined exactly when the consolidation ends and the strategy’s edge returns.

Boredom Increases Activity

Strangely, quiet markets often produce more trading, not less. Small intraday moves start to look meaningful. Short-dated options look tempting. Leverage sneaks back in. The phrase “it’s bound to break out soon” appears with increasing frequency.

Consolidations can feel gradual. Breakouts rarely are.

ITM OUT Signals

SPY hasn’t triggered an ITM signal. Not even close. QQQ, however, has triggered a new OUT signal – part of the updated rules in the forthcoming ITM book. Same consolidation phase, but different structure. QQQ is quite a different beast to SPY and has different rules. It moves faster and is more volatile. It reacts more aggressively to shifts in narrative. A similar sideways move at the index level does not mean identical underneath.

The Real Risk

The real risk in consolidation is not missing a breakout. It’s abandoning discipline out of boredom. Markets move in rhythm: expansion, contraction, expansion again. Long bases often precede meaningful moves. The longer the compression, the more significant the eventual release tends to be. But that only benefits those who are still following their rules when it happens.

“How did you go bankrupt?”

“Two ways. Gradually, then suddenly.”

(Hemingway, The Sun Also Rises)

Consolidation Is Dull

Consolidation is dangerous because it’s dull. When the market is boring, restraint is the edge. And boredom is where most traders quietly lose it.

How long is it going to last?

Obviously I don’t know, but SPY consolidation periods have typically been shorter than this one. The longest one in recent years that I could find was on 2015 when SPY went sideways for 7 months, trading in a tight range of $205 – $215.

This one is already testing patience. Which is precisely the point. Boredom is not a signal. It’s a test. When nothing is happening, your rules still are.As the saying goes:

If your trading isn’t boring then you’re doing it wrong.

To the markets . . .

I’ve explained what is happening in the markets generally already, but let’s look at the charts.

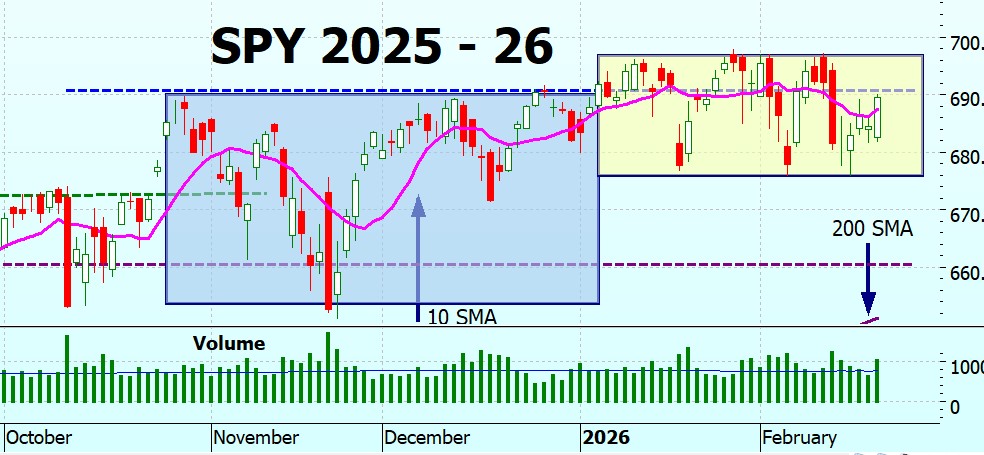

SPY Charts

On the long term chart the new trend line we drew in seems to be holding.

SPYG Charts

SPYG still in its trading box. Note that the 200 SMA is now over $100 and there is only a 4% difference between them. If SPYG breaks to the downside we may see a death cross.

On the long term chart SPYG is well out of its trading channel and heading sideways. I’ve drawn in what may be support (but it is a bit early to say – it may not hold)

QQQ Charts

The QQQ is definitely in that Darvas box, trading sideways. I’ve mentioned above that the new book has a QQQ bull strategy – and that it has triggered an OUT signal. It isn’t exactly the 10/100 cross, but it is near enough for our purposes, and I am giving the heads up before the book is published. I’m out of all QQQ options, but it is without any great satisfaction – I am hopeful that QQQ is going to bounce and start climbing – but that is only my feeling, not borne out by anything in the charts. Feelings don’t count in the market.

On the weekly chart you can see the sideways movement (blue line)

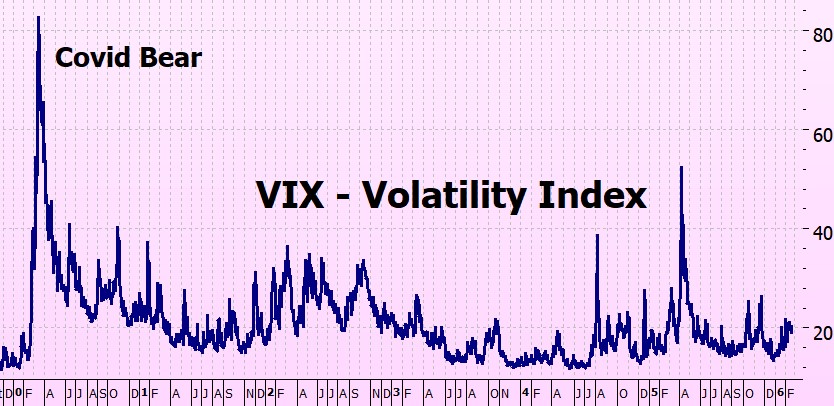

VIX Chart (Volatility)

Nothing much happening in the VIX.

ITMeter

SPY & SPYG

QQQ

The week ahead. . .

NVDA Earnings

The big news of course is that it is NVDA earnings week. The NVDA chart for the last 2 years shows something interesting: trading volume has decreased markedly, around 40 – 50% below long term norms. Should we be worried?

Probably not. Many tech stocks have shown this pattern as they mature int core holdings:

• Apple volume peaked around 2012–2013

• Microsoft volume fell after 2015

• Amazon volume declined after 2018

WHY? Because of reduced speculative churn. Options trading increasingly replaces stock trading, and NVDA is now one of the most actively traded in weekly options, 0DTE options and spreads, all of which reduce share volume.

Buy-and-Hold ownership has increased:

• Index funds (S&P 500, Nasdaq-100 ETFs)

• Institutional long-term portfolios

• Pension and sovereign funds

These holders trade infrequently. When ownership shifts from traders to institutions, turnover drops even while price rises. Falling volume in a leading stock often means ownership is becoming concentrated.

NVDA used to be heavily traded. Now it is heavily owned.

Earnings & Announcements

Monday, Feb 23:

Economic Data: Flash PMI (Manufacturing & Services), Chicago Fed National Activity Index.

Tuesday, Feb 24:

Economic Data: Consumer Confidence, Case-Shiller Home Price Index.

Earnings: Home Depot (HD), Lowe’s (LOW).

Wednesday, Feb 25:

Major Earnings: Nvidia (NVDA).

Other Earnings: Salesforce (CRM), Dell (DELL).

Thursday, Feb 26:

Economic Data: Weekly Jobless Claims, Preliminary GDP (Q4).

Friday, Feb 27:

Economic Data: Core PCE Price Index, Personal Income & Spending, Consumer Sentiment.

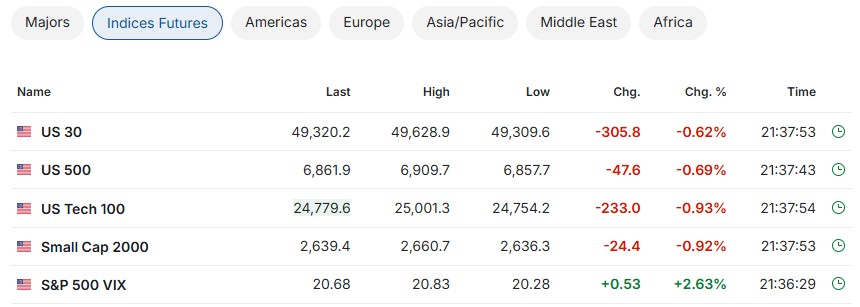

The Futures

Are having a major conniption – likely reflecting uncertainty after the U.S. Supreme Court decision limiting the use of emergency powers to impose tariffs. The ruling does not necessarily change trade policy immediately, but it introduces uncertainty about what tariffs will ultimately look like and how they will be implemented. Markets typically dislike uncertainty more than the policy itself, which is probably what we are seeing here:

Fingers crossed for a good week!

Heather

Trade the tide – not the waves

Q & A

Related Posts

- Why Bother?

Why bother with charts? It was a question that set my back on my heels…

- AI: Hype & Bubble?

AI: Is it all Hype & Bubble? The market went down last week (until Friday),…

10 Responses

Dear Heather,

Regarding the Iran war going on right now, hopefully the stock markets around the world will not be going down too much on Monday when the market opens on March 2 of 2026. Please be safe and respectful and responsible (schools motto).

HI George Henry!

I look at the Iran situation in this week’s blog and see what happened last time. I don’t think it will be as bad as people are expecting – but that’s just my opinion!

Fingers crossed.

x

h

Dear Heather,

I read your weekly blog because I am deeply invested in the strategy you have devised. I think the content is very substantive, but the graphics are truly magnificent! Your enthusiam is contagious. Please continue to inform us with your informative and entertaining content.

Bill

Thank you William!

Your lovely comments are very much appreciated!

x

h

Fascinating information about the volume peaking on various stocks. That is new information to me. Thanks for that tidbit. “Turnover drops even while prices rise”.

Hi Kate!

Yes, on first glance the turnover looks worrying, but when you think about it and do some digging it all becomes clear!

x

h

Heather,

Hope you’re healing up nicely from surgery. Probably have another 3 weeks on crutches I assume. I did purchase both your bull and bear books. As I follow the blog, I probably exited QQQ a week after you did. I know you mentioned the new bear version is easier to follow. I’m looking forward to that. Could you share exactly when the new books will be released? I am looking forward to updating my collection and don’t want to miss the QQQ signal should we need to get back in.

Regards,

Anthony

HI Anthony – should be using crutches, but am shuffling around without them a lot of the time. Feels a lot better.

I’ve just received the proofs today – so will be aiming for 2 weeks time to publish.

But don’t worry – if there is a QQQ IN signal I will publish it here – I won’t keep it a sercet from my wonderful readers!

x

h

Great analysis and commentary!! You per your usual put things in perspective!

Thank you Heather!

Thank you Andrew – glad I helped!

x

h