AI: Is it all Hype & Bubble?

The market went down last week (until Friday), and much of the drop was due to AI stocks. Why? Because a report was published, producing scary headlines:

MIT study shatters AI hype: 95% of generative AI projects are failing

95% of firms gain zero return from generative AI investments

95% of companies see little to no tangible results

Tech Sell Off

The Nasdaq went into a decline but was this justified? Let’s have a look at the actual report. Yes, it found that 95% of generative AI pilots fail to deliver any measurable financial impact. Only about 5% of projects result in rapid revenue growth and scaled adoption.

The Hype Cycle

Now, why would this be? First, let’s review the AI Hype Cycle adapted from Gartner’s new technology implementation ‘hype cycle’.

Where are we now? Well, we’ve definitely fallen from the Peak of Inflated Expectations. We could be in the Trough of Disillusionment, but I think we are just climbing out of that onto the Plateau of Productivity.

Integration Gap

Any new technology starts with inflated expectations, and worse, people who have really no idea about business processes are the ones fanning this. I hate to say this about my ex-profession, but many in IT have only the vaguest idea of why the business uses IT systems.

Likewise, very few in business know what IT can and can’t do but that never stops the marketing or PR department! Naturally, their suggestions / recommendations of how to use the new techology are usually way off the mark.

The Root Cause

Adopting a new technology requires both business and technical knowledge. We’ve all known senior executives with wacky ideas about what technology can do and where to use it. Is this the case here?

All Sizzle, No Steak

The study found that most companies experimenting with generative AI are channeling budget into sales and marketing gimmicks – chatbots, customer engagement toys, lead generation, campaign content). They look flashy, and make headlines. They’re what we hear about.

These are high-visibility but low-return projects — they rarely move the profit-and-loss needle. So, what does move the needle?

Where is the ROI?

The MIT report points out that the real returns are hiding in the boring stuff: automating back-office tasks, cutting outsourcing bills, and streamlining compliance. In other words, the hype is front-of-house, but the value is in the plumbing.

Remember the banks?

When the banking system introduced IT they focused on labor intensive back office processes, handling vast amounts of transactions with fewer clerks, and so cut costs and reduced errors. This drove the productivity gains, enabling the later customer-facing technologies like ATMs and online banking.

What about retail?

The same scenario here: barcode scanners and POS systems replaced manual price entry and inventory tracking. This laid the groundwork for online shopping, not a sudden leap but the natural step of IT-driven automation out of sight of the customers.

What about AI?

I can’t help but think that we are ignoring the lessons of the past. Instead of using AI in back office processes we’ve gone right for the flashy stuff. And guess what: it doesn’t work. The showy front-end applications have proved to be more about image than impact.

Chatbots, automated marketing campaigns, AI-drive engagements look innovative and get headlines, but in reality frustrate customers with clunky interactions. They don’t improve the customer experience or the bottom line.

What's ahead for AI?

I still think that AI is every bit as transformative as the Internet. Yes, it has been hijacked, but I think that this is temporary, and that when businesses give up the ‘gee-whiz’ applications and look logically at how to use AI it will totally transform businesses. .

I think we are in the ‘trough of disillusionment’, but seeing the ‘slope of enlightenment’ and am sure we will finally get to that productivity plateau.

But the Stock Market?

Translating that into stock market terms, I think that AI stocks will out perform; which ones I don’t know. That’s why an ETF like QQQ, which like all indexes, is self-correcting, is a good idea. In my next book (yes, I’ve decided to do it) I will include QQQ.

Continuing the AI theme

I’ve been experimenting with some AI-generated materials. I uploaded last weeks blog to it and instructed it to make a chat between 2 people about it – strict instructions to stick to what I had written, no gratuitous comments or ‘market wisdom’.

What do you think? I thought it was pretty good, and I haven’t yet tested the interactive bit of this where you can ask questions and direct the topics. Do let me know via the comments if this would be a good thing to do every week so that you had a choice of media.

<later> Here is the audio of this week’s blog. Let me know what you think:

Coming out of Shadow

I’ve decided to do one last book, transform the website and blog, and come out of hiding. When I stopped work, I vowed I would never have a boss again, so started a business. Then I realised that customers could be just as unreasonable and annoying as bosses, so when I closed my business in 2018 I vowed never to deal with customers again. Hence the absence of profile. I have deliberately stayed in the background, and dealt with everyone at arm’s length.

But now I have decided to give it a go, and have agreed to do a podcast and some interviews. I will post details of them next week.

I may introduce a part of the website to interact face-to-face with traders. What do you think?

To the market

Monday to Thursday was dismal, but Friday was quite a bit different. Let’s check the charts.

SPY Charts

The hesitation on Monday was palpable; a doji and extremely low volume. There were few traders, and the ones who did trade couldn’t make up their mind. The next day they decided – down, but the day after while the bears started driving the price down, the bulls rallied and drove them back up forming a dragonfly doji, on high volume. The next day was a sitting-on-the-hands day, doji on low volume. Of course, everyone was waiting for the Jackson Hole announcement.

Friday – a lovely day on high volume, making up all the losses of the previous 4 days.

On the long term chart everything looks nice. I thought that I would put the volume on it. You can see that the highest volumes are always when there’s a bear, but what is encouraging is the general volume increase since February this year.

SPYG Charts

SPYG has a similar pattern to SPY, although it hasn’t quite made up the week’s losses – see QQQ for explanation.

On the long term chart we can see that it still hasn’t made it back into its trading channel.

QQQ Charts

QQQ ha a similar pattern to SPY but hasn’t made up the weekly loss, and isn’t back at the high it made a couple of weeks ago. It looks as though support may be forming at the 560 level (pink dashed line).

On the long term chart we see it bumping along the bottom of the trading channel.

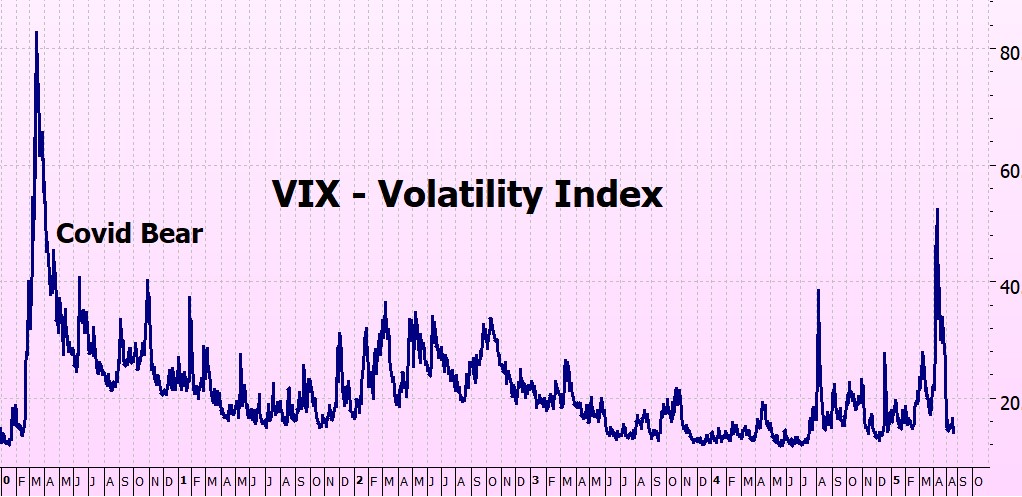

VIX Chart (Volatility)

The VIX is comfortably below 20, the low volatility threshold. The market moves this week were not large and withing recent the trading range so the VIX was not hugely affected.

ITMeter

The week ahead . .

The Fed was the big news last week, and it turned out to be a nothing-burger, with traders back to an 85% chance of a September rate cut.

This week the big news is, of course, the NVIDIA earnings, due on Wednesday. Expectations are 53% revenue growth to $45.8b and EPS of $1. Pretty high expectations! It they are not met then there will be a big tech sell off. There are also some lesser techs reporting this week.

Friday sees the PCE (personal Consumption Expenditure) for July. Expectations are:

Headline PCE (overall inflation):

- Forecast to rise 2% month-over-month

Core PCE (excludes food & energy):

- Expected to increase by 2% month-over-month and 2.7% year-over-year, slightly above June’s 2.6% level

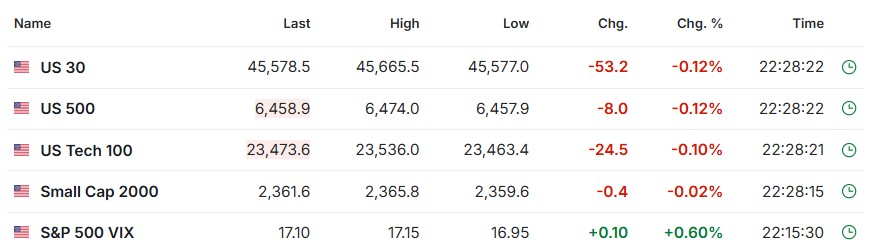

The Futures

The futures are down slightly (to be expected after Friday’s rise) and it is still 11 hours to market open.

Fingers crossed for a good week!

Heather

Trade the tide not the waves

Q & A

Related Posts

- AI: Bubble or Hype?

AI: Bubble or Hype Cycle? Tariffs and market volatility are starting to become the new…

- The AI Hype Cycle

Where is AI on the Hype Cycle? Many of you will know about the Hype…

- Side Effects of AI

Unintended Consequences of AI. There’s a side effect of the ‘AI Revolution’ that I’ve been…

24 Responses

Outstanding job – please keep it up. On the Darvas Box article, many have tried to use it but later books noted (1) Darvas weekly screening of Barrons flagged the issues involved in new technology (what we would call high growth small caps) and (2) Darvas limited his selections to a manageable number. Using his Box approach he implemented a buy the dip tactics for selected issues. The Box reduced the number of whipsaw buy and sell actions.

Hi Ronaldo – thank you – yes, you have picked up on a point that I felt was not explained by the book: the first being how did he select the stocks in the first place?

As for using the Darvas box to trade – I have never used it for trading decisions (well not since an early experiment many years ago – not successful), but often use it so that I can ‘see’ more clearly what is going on. Its a useful tool, not the be-all-and-end-all of trading decisions.

thanks!

h

Heather,

I liked the bot chat, but, I too, prefer to read. I would love to interact face to face. I would like to hear your voice explaining your process. I love that connection, but, honestly, from what youve just written, I feel like you could begin to resent the obligation. Only you know yourself and how you value your time. Please, YES! Write the book – I cant wait for that. But you have worked hard to live your life on your terms. Protect that.

And thank you for leading the way for your readers to do the same.

Many blessings. Uncle Dave

Thank you so muchDave!

x

h

Content below is generated by AI, but I wrote the prompt myself and the idea is from me instead of AI.

Hi Heather,

Following up on our conversation last week, I wanted to elaborate on why I think futures might be a compelling alternative to deep-in-the-money (ITM) call options for our strategy. While options have their place, I believe futures could be more efficient here.

Here’s a breakdown of the trade-offs as I see them.

### 1. Risk Profile (Practical vs. Catastrophic)

You’re right that the “unlimited risk” of futures is often overstated in normal market conditions. An S&P 500 drop of 20+% in a single day is nearly impossible due to market-wide circuit breakers, and our strategy’s exit signal would trigger well before that.

For a deep ITM call, the delta is near 1.0, so in a typical 15-20% drop, the financial loss would be almost identical to a leveraged futures position. The key difference isn’t day-to-day risk, but **”tail risk”**—an extreme, overnight event.

* **Options:** Offer true limited risk. If a “black swan” event caused the market to gap down 40% overnight, your loss is capped at the premium you paid. It’s essentially catastrophic insurance.

* **Futures:** In that same gap-down scenario, your loss would not be capped. It would blow past any stop-loss and could result in losing more than your initial capital.

So the trade-off is: options provide better protection against a catastrophic, though highly unlikely, event.

### 2. Simplicity and Management

At first glance, futures seem simpler: no Greeks (delta, theta, etc.) and no strike prices to choose. However, they come with their own management tasks that options don’t have:

* **Margin Calls:** Futures are “marked-to-market” daily. If the position moves against you significantly, you may need to add cash to your account to meet a margin call and avoid forced liquidation.

* **Contract Rollover:** To hold a position long-term, you need to “roll” the contract every quarter (sell the expiring one and buy the next). This is an active task with its own transaction costs.

By comparison, buying a long-dated call option (LEAPS) is a one-time transaction. You pay the premium upfront, and there is no further margin or management required until you decide to sell or it expires.

### 3. The Strongest Case for Futures: Cost-Effectiveness

This is where futures have a significant and clear advantage. Based on my analysis, they are structurally cheaper for holding leveraged long exposure.

Here’s a breakdown using some reasonable assumptions:

*(Assumptions: 3x leverage, risk-free rate: 4.3%, S&P 500 dividend yield: 1.1%, call option bid/ask spread: 0.5%, call option time value drag: 2.5%, interest on uninvested cash: 4.3%)*

* **Call Option Annual Cost:** (Time Value Drag + Spread) * Leverage

(2.5% + 0.5%) * 3 = **9.0%**

* **Futures Annual Cost:** (Cost of Carry * Leverage) – (Interest Earned on Your Capital)

(4.3% – 1.1%) * 3 – (4.3% * 1) = **5.3%**

This cost difference of **3.7% per year** comes from two main factors:

1. **Futures benefit from dividends:** The price of a future already accounts for the dividends paid by S&P 500 companies, which is a direct drag on a call option’s performance.

2. **Your cash earns interest:** With futures, you only post a small margin. The rest of your capital can sit in your account earning interest. With an option, the entire premium is a sunk cost that earns nothing.

### Summary

The choice really comes down to what you want to prioritize:

* **Choose Options if:** Your primary goal is absolute risk limitation (protection against catastrophic gaps) and you prefer a simpler, “set-it-and-forget-it” management style.

* **Choose Futures if:** Your primary goal is maximizing returns by minimizing annual costs, and you are comfortable with the active management requirements (monitoring margin and rolling contracts).

Given the potential **3.7% annual performance advantage**, I lean towards using futures, but I wanted to lay out all the trade-offs.

Let me know what you think!

Hi Tyler – I actually wouldn’t go for either of them.

1) 3 times leveraged options do not perform well over time – the back testing has shown that around 60%s strike is optimal over the long run. I get that shorter periods have better results with a higher strike, but they can go disastrously wrong on a sudden drop.

2) Futures – first of all, I don’t have a futures account – and have never felt moved to have one. They probably wouldn’t approve me for it anyway as I have no financial qualifications – and have no intention of getting any (they seem to rot your brain IMHO! – OK thats a bit harsh but most people I know with financial qualifications are not markedly richer than average)

But futures are just too risky for me – I prefer a more calm life, that allows me to travel for 4 months of the year!

h

Regarding the 2 Bots interview. I think it was spectacular! I felt all the summations were excellent and worthy of note taking as if I was in your classroom! Excellent, as are all of your commentaries.

Hey Andrew – great, glad you liked it. I thought it was pretty good also. I’m just going to select the non-chart-reading part of this weeks’ blog and see what it can do with that.

Thanks!

h

Thank you for deciding to do the new book. Just curious, do you have any idea how long you think it will take? I totally understand that this will take time 🙂

HI Brian – I think 3 – 6 months – expect 3 months to write, and then 3 months to much around with all the setting out etc (I can’t get anyone to do that because the text has to match the images and not leave blanks – its a very boring job but not as boring as having to check and correct what someone else has done.)

I keep on thinking that it would be a nice round point to be able to do the backtesting up until the end of the year, but I’ll have to figure how that fits in.

Sometimes I think I am crazy, but I would like to streamline the books, have everythong on one place, color, and have thee wensite to match it so that I don’t clutter up the book with too many charts.

Still figuring . .

h

I would love to see you with a youtube channel. Audio is great bu – no charts. I look forward to seeing whatever content you produce.

Hi ‘A’ – yes, I left out the chart bit, I can’t figure out how to do that properly – you have to actually see the charts. Any ideas gratefully received.

h

Hi Heather,

I listened to the AI generated chat last week when you put it at the bottom of your blog post. I prefer reading your insights on what the market is doing currently but enjoyed the bots chat on protecting profits. Maybe you could use them to go over something you think readers could benefit from. I would love if we could interact with you face to face and/or listening to any podcast you do!!

Hi Charity – I, too, prefer reading as it is quicker (people talk so slowly – I always have things on 1.5 speed, so they all sound a bit like donald duck!) and I have a bit of a photographic memory for things – but different people prefer different ways and at different times. I’m just going to give it this week’s blog and see what it does with it – and I will try the interruptions to see how it handles them

Face-to-face – I am still pondering it, I am not sure what it would add that I couldn’t do better in print – but we’ll see how the podcast and interview go.

x

h

Looking forward to the new book! No pressure…lol

Hey Blake – part of the reason I announced it is that I now know I have to do it.

h

Hi. It’s been a while since I read the book. Outside of a lower share price, why couldn’t we follow your strategy by using SSO, the leveraged SPY ETF?

HI David – I never recommend leveraged ETFs – in both the bull and bear books I explain why and caution against using them. Here’s an early posts I wrote about them: https://heathercullen.com/why-not-use-a-leveraged-etf/

and i;m sure i have done a more recent one, off to search for it. Damn, can’t find it, Must redo the blog with a decent index.

But in the latest edition of ITM Bull it is in Chapter 12: Leverage and Protection. There is a whole section on the dangers of leveraged ETFs.

Hope this helps

h

On the long term chart of the Spy 20 – 25 … the channel ( where we are ) has no resistance ( heard the chatter that we’re heading to 7000.00 )… the Head Lemming ( was yelling “ stone her “ ) now He’s saying “ march “… what stage of a “ market cycle “ are we in the Head Lemming asks “ the Lady “in the red book mobile ?

r

pipes… really! Stone her.

Randy, you are getting really obscure!

The SPY 2020 – 2025 has a trading channelstarting in April / May 2020, and is currently reading lower bound 520 upperbound 675 (approx). IN the daily chart we have a new high (645.31) which beats the previous high (644.95 on 14 Aug) so there is no resistance as yet.

Market cycle? depends on which cycle you are using, if it is the Investment clock then I would suggest that we are after 7 (falling interest rates) after 8 (rising share prices). After 9? (Rising commodity prices) – the Invesco DB Commodity Index Tracking Fund (Ticker: DBC) has been in decline sincemid-2022 – although maybe that is the wrong index.

Just to refresh you:

The Market Cycle “Clock”

6 o’clock → interest rates falling, early recovery, credit picks up.

7–8 o’clock → equities strongest, growth accelerating, earnings expanding.

9 o’clock → commodities rise, inflation builds, late-cycle dynamics.

I would suggest that we are between 8 and 9 O’clock, where 9 is the end of ‘recovery’.

Which means we have not yet started the ‘boom’.

Does this make sense / answer your quesiton?

h

10–12 o’clock → rates rise, growth slows, equities roll over, leading toward recession.

Heather ,

Wahoo another book ! That’s awesome, can’t wait! The simulated chat about last weeks blog was just like listening to a podcast, pretty cool

Thank you Joe . . .now to find time to write it!

h

I heard that AI could write it for you ;o)

Hey martin – yes it could, but I wouldn’t put my name on it!

h