Different SMAs.

Now that we are sitting on profits people are starting to think about how to protect them. Our golden cross came in mid-May, and we got in around $590. SPY is now trading around $645, a 9% increase, which means that at a 50% strike ($323) you would have an 18% increase, more if you had a 60% strike.

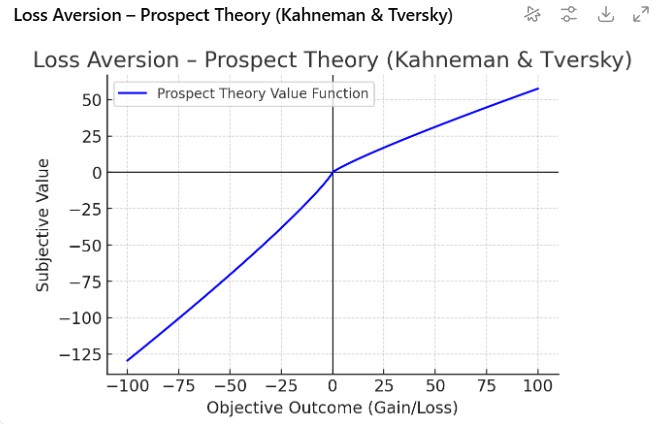

Loss Aversion

Prospect Theory shows that the psychological pain of losing is about twice as strong as the pleasure of an equivalent gain. As an example, the negative emotional impact of losing $100 is about 2x stronger than the positive impact of gaining $100, which means that the urge to protect your profits is strong. Graphically:

Avoiding Drawdowns

I am afraid that drawdowns are an inevitable fact of life when you are a trader. This is reality, and the market doesn’t feel the need to conform to our wishes. Let’s be clear on some terminology here:

- A LOSS is when you close a trade for less than you put in.

- A DRAWDOWN is the peak-to-trough in your account.

So, for example, if your account was at $100,000 and the market went against you it might drop to $85,000. That’s a 15% drawdown. However, if you had bought in for $60,000 then you would also have made a 42% profit. So, remember:

DRAWDOWNS are NOT the same as LOSSES

However, traders don’t like either drawdowns or losses, and are constantly worried that their profits will disappear.

What ITM Does

ITM helps you avoid the worst of market downturns, and strikes a balance between telling you that there’s a serious downturn without whipping you in and out of trades. In other words, we:

Trade the tide, not the waves

Different SMAs

But people want to avoid drawdowns, so let’s look at the most frequently-suggested action, which is to have a tighter rule to get out and get out on a tighter cross, a more sensitive indicator. For example, why don’t we get out on the 5/50 cross? That’s much more sensitive. However, the question then is:

When do we get back in again?

Once we are out following a 5/50 death cross, when do we get back in? If we wait for the next 10/200 golden cross we may be waiting a long time – years, possibly.

Here’s what happened in 2020/2021. The golden cross got us into the market in early June 2020 (after the covid bear). The 5/50 death cross got us out in early September, avoiding the dip for the rest of September. But the 10/200 cross was still in force – we were still in a bull market. So when should we get back in? The next 10/200 cross was in 2022. Would we be happy sitting out for 2 years?

The logical answer is that is we want clear, unambiguous signals we have to trade the same SMA parameters getting in and out. So how would we fare with the 5/50 SMA cross?

For a deeper discussion of this please see the blogpost Why Backtest?

Trading the 5/50 Cross

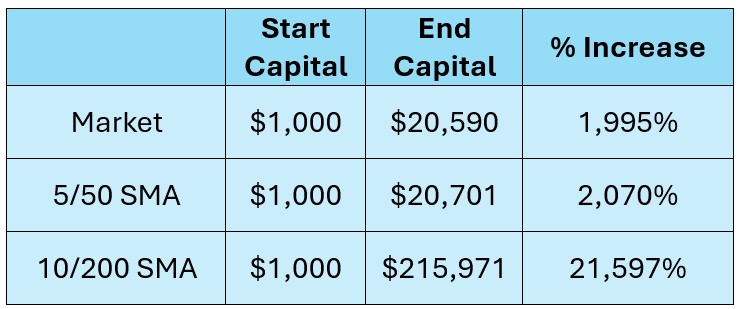

Running the 5/50 SMA combination through backtesting from 29 Jan 1993 to today, using a 60% strike, we get the results:

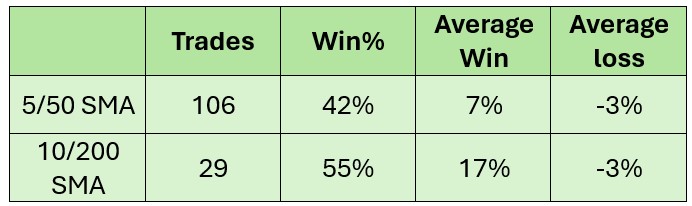

The 5/50 SMA barely beat the market! How can this be? Why such an enormous difference? The explanation is in the trade data:

With the more sensitive 5/50 you trade more often, but your winning percentage is less than 50% – not good odds. But more than that, look at the average win: 7% compared with the ITM 17%. That’s what makes all the difference. Even through the average loss is the same for both strategies (3%), the number of losses is greater with the 5/50.

Other combinations

You have 2 choices:

- You can take my word for it that I have tried practically every combination and found the 10/200 to be the best; or

- You can create your own backtesting system and check. The instructions are here: https://heathercullen.com/backtesting/ in ‘Download ITM Backtesting Documentation’.

Backtesting

All the documentation is there, if you follow it you can create your own, Please don’t ask me to send you a copy of my working system. I did that early on in the piece and totally regretted it as there is then a requirement to provide support and training, so no more, that’s not what I want to do.

Backtesting Systems

You can use other backtesting systems, but I haven’t found one where you could put in the all the rules we use: choosing strikes, cash management, rolling up and out, whitespace, etc, and having them as variables. If you do use another backtesting system your results won’t be exactly the same, but they should generally show similar results. You can also share backtesting ideas on ITM Chat.

To the markets . . .

A nice, uneventful week. No nasty surprises, no out of control euphoria. I can handle that!

SPY Charts

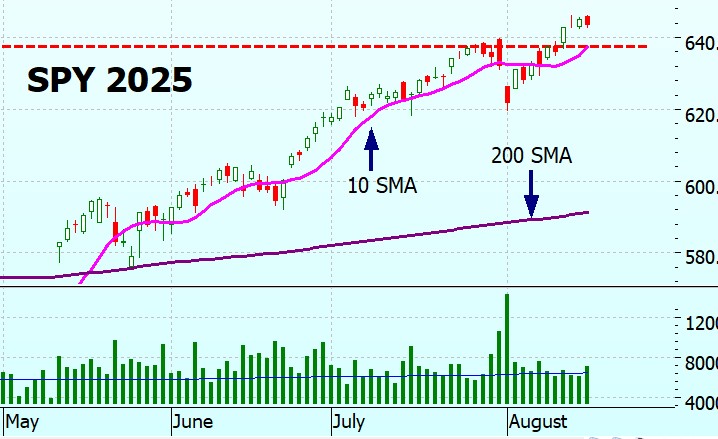

SPY broke through the previous high made in late July and is headed upwards. The volumes are around average, so it doesn’t look as though it is running out of steam yet. Famous last words. I really shouldn’t say things like that; it is tempting fate.

On the weekly chart we see the uptrend, and indeed the trading channel, is still intact. For those who are nervous and think that SPY has risen to far too fast, have a look at the bull run starting in March 2020. By the time it stopped in January 2022, it had doubled.

If we look at the current bull run, it started in May when SPY was around 500. That means to match the performance of the 20-21 bull run SPY would have to get to 1,000. That would be nice. But we’re not anywhere near there yet.

Am I saying that we are definitely going to get there? No. I have no idea, neither does anyone else. I am just pointing out what is possible because it has happened before.

SPYG Charts

Woohoo!! SPYG has made it over $100. Nice. It has been making new highs, just pausing a little at the $100 level.

On the weekly chart we can see that it is just crawling along the bottom bound of the previous trading channel. Let’s hope it gets back in.

QQQ Charts

QQQ has also been making new highs this week.

On the long term chart, it is back in its trading channel. See SPY for further comments relevant to QQQ also.

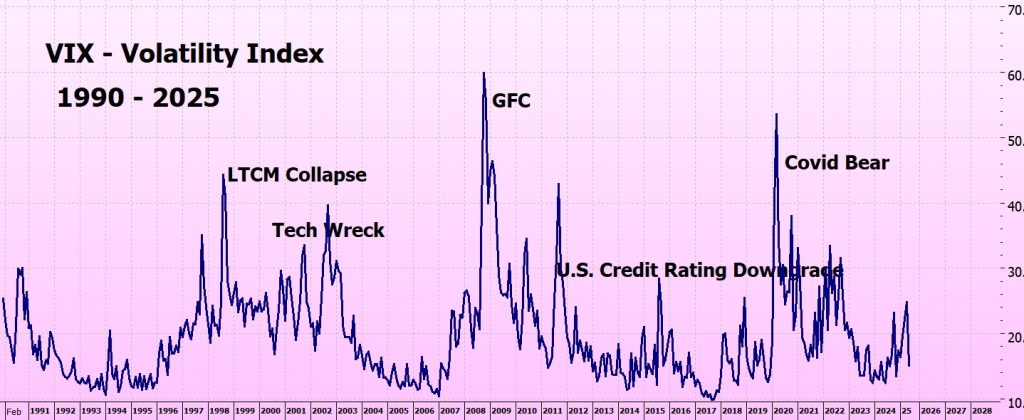

VIX Chart

Hmm. Not sure if I should bother with this. I inadvertently left it out last week and no-one let me know. Here it is anyway, a long term view of the VIX.

ITMeter

The week ahead . . .

Reporting season is coming to a close, with S&P 500 companies delivering 12% profit growth, which beat the 5% consensus expectation. One of the interesting ones to report this week is Zoom. Remember that when it was a market darling? The dizzying heights it reached? How is it faring now?

The large retailers are reporting. Walmart, Target, Home Depot, and Lowe’s are closely watched for signs on consumer spending and inflation.

The Fed are at it again – they are at Jackson Hole on Aug 21-23, so everyone will be hanging out to find out about rate-cuts. The rate decision is made on the second day of the meeting, and is released at 2:00 p.m. ET. A press conference by the Fed Chair typically follows at 2:30 p.m. ET.

I imagine there will be a bit of a fuss about the resignation of one of the Governors, Adriana D. Kugler, resigning and so there is an empty seat. The replacement, Miran, will not be at the meeting as the Senate must confirm him which will not happen until September at the earliest.

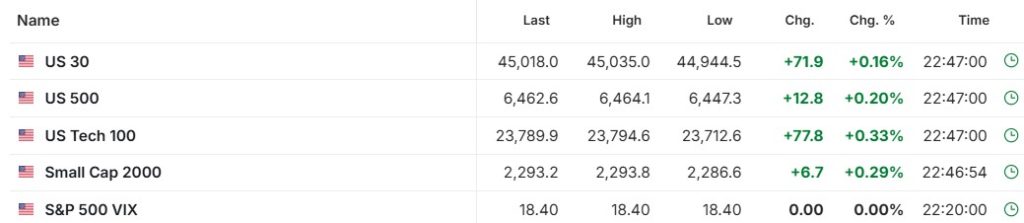

The Futures

The futures are up a bit, but it is still 10 hours to market open.

Fingers crossed for a good week!

Heather

Trade the tide, not the waves

Q & A

TESTING AREA

Hi! I’m testing out various ideas for add in features. Please feel free to try them and let me know what you think via the comments.

Panel discussion on Protecting Profits

Mind map on blog

Blog Quiz

Blog Summary

Blog Glossary

Related Posts

- Riding the Bull

Riding the Bull. Readers are getting twitchy. ‘Shouldn’t we get out now? We’ve made profits,…

39 Responses

Hello Heather, I enjoyed the new panel discussion audio. I didn’t really find the other parts useful, but others might. You could move the audio up to the top of the page since it doesn’t take much room. I’m guessing it’s all AI generated??? Have a great day, Michael

HI Michael – thank you for the feedback – it was a bit obscure right at the bottom of the post, so I have moved it up to be more visible this week and hopefully get some more feedback.

Thank you for taking the time to let me know.h

One thing I have learned is that, when you are considering scaling in and out of a position, you have to treat those entries and exits as separate systems, even though they are using the same basic indicators.

As an example, let’s consider the Turtle Trading system. Entries on 55 day breakouts and exits on 20 day closes with a scaling in at 1/2 ATR increments. Although presented as one system, what you really have is 4 separate systems which need to be evaluated on their own merits. They all exit on the same signal but actually have different entries.

One entry is at the breakout, another is 1/2 ATR past the breakout, another is 1 ATR past the breakout, and the last is 1.5 ATR past the breakout (if I did my math right). Each of these entries must be evaluated independently to see if they are profitable, and, in the end, the best method would actually be just to drop the worst entry criteria and stick with the best entry with 4 times the position size.

Hey Micheal – seems logical to me.

I have always found that the more complicated I get the less profitable I am!

h

Heather, since your option price is now less than 45% of the total, have you rolled out and up? If yes, did you buy a 6 month or 12 month option?

HI David – I have several accounts and lots of options bought at different times so can’t answer definitively.

But yes, I would start to think about rolling – certainly when it got to 40% I would have already rolled.

6 month or 12 month? I (peronally) would probably go for 6-8 months, but that is beacuse I am on the market every day. 12 months is nperfectly fine is you only check on weekends.

Hop this helps.

h

Hi Heather,

I apologize. I just saw your answer in last week’s blog. So, you can disregard this post. Thank you for answering! I appreciate it!!

OK, no prob!

h

Heather, why did you choose SPYG as a lower cost ETF to use rather than SPLG? SPLG invests in all of the same stocks as SPY, while SPYG is a bit different in that it invests in S&P 500 growth stocks. Granted, SPYG yield has consistently beaten both SPY and SPLG, but SPLG would be a better match to SPY. Ultimately, either one would be good, lower cost alternatives to SPY.

Hi Jimbert – it was practicalities.

SPLG is much more lightly traded so the spreads are wider. For example, the March 2026 options for a 60% strike are:

SPLG: Strike 45, Bid / Ask 29.10 / 31.9, 9.62%

SPYG: Strike 60, Bid / Ask 39.40 / 41.00 4.06%

The spread of almost 10% means that you have to move that much before you are in profit. I would like it if the SPYG spreads were as small as SPY, but it was the most reasonable substitute I could find.

If this doesn’t make sense please get back to me.

h

That makes total sense. Thank you!

Heather. Hey

I have really enjoyed traveling vicariously through your posts. Thank you again for all your in depth work and for sharing your experience openly in your blog. I hope you are feeling refreshed and ready to let your engaging creative style flow into your next book. I look forward to it. I have given copies of ITM to friends, and also to our grandson with whom I have found common ground in this fascination with options. Your work has given me a great new perspective on trading overall. I trust you and your experience, and I am a student of trading, so I assume you have good reasons for not talking about trading Credit Spreads on these Index ETF Long Calls. I know, “The Market is not for income. It is for growth.” (Who said that?) It does seem such a shameful waste to leave all that instant gratification just lying there. Like the cat with the coins pictured above.

I’m guessing there’s a lesson here and a good story behind it?

Hi David,

just checking that I understand – you are thinking credit spreads instead of a straight option?

Yes, you can do it – but I’ve never found the trade-off to be worth it. If you use a high enough strike to make sure that you don’t miss out on a big market move then your premium is very small.

I’ve nothing against the idea – just never seen it work well in practice.

If, on the other hand, you mean that we already have the SPY shares / DITM options – then I understand and I am playing with that at the moment trying to make it work, with little success so far.

Here’s a coupld of blog posts I have done on this:

https://heathercullen.com/covered-calls-revisited/

https://heathercullen.com/are-covered-calls-worth-it/

Hope this helps

h

Heather, Thank you for getting back to me. I think of you as my mentor. I study your books, follow your blog, AND I can ask questions and you respond. (Or was that from ChatGPT?)

Either way, I could get used to this.

Yes. Diagonal Credit Spreads or Calendar Spreads. I was hoping you had addressed “Poor Mans Covered Calls” at some point. My results so far have been encouraging.

BTW, I tried to save you the trouble by entering several key words in your search window but all came back wanting. How do I look up past articles by topic?

Thank you again. I appreciate your attention.

UncleDave

HI Dave – no, all my asnwers are really me – I use GPT for research and formulas only!

I realize that the blog has become unweildy, and the search is not much good. Right now I am searching for something myself – and using google as it is quicker e.g. ‘Heather Cullen Blog Why Backtest’

Re calendar spreads etc – yes, I must revisit all that.

I am using GPT to help me download all the blog posts for the last 4 years, separate out the ‘evergreen’ content (,e, not the chart reading bit) and index it properly – I need an uninterrupted day for it and that has proved impossible this week. Hopefully next week. Its actually a big job, I am surprised about how much I have written.

So – a solution is coming, but probably 2-3 weeks away.

Hope this answered your question?

h

Heather, you ARE prolific.

I look forward to talking more about calendar spreads. Until then, I will be refining what, so far, is working well. I hope to bring something useful to the conversation.

God bless.

UncleDave

Heather, thank you for the insightful article. I fully trust your backtesting on the 10/200 averages being the most profitable. For me it comes down to a balance of risk management and wanting to maximize/preserve gains. If I understand your methodology its all in at golden cross and all out at a death cross. I plan to use your back testing approach to see if there is a combination of crossovers that might signal a time to scale in as market starts to move off of lows as we approach a golden cross and conversely a point to consider scaling out of the market as the trend begins to turn down from the top as it starts moving down instead of waiting for the death cross and then getting out.

For example if we are all cash during the uncertain days of a bear market is there a signal before the golden cross where it might make sense to risk 20% of account to buy ITM options to catch some of the gains as the market starts its move to a golden cross. And when a bull run starts to lose steam, is there a signal that might make sense to start taking partial profits by selling some of your positions. I have some homework to do. Thank you for your insights and the ITM strategy it has been an amazing game changer for me. For now I am just following the plan.

HI David – that is the strategy used by Jesse Livermore – stepping into trades. I’m just in the middle of a book by him ATM, I’ll do a blog on it when I have finished it, digested his strategy, and check how it works today.

Give me a couple of weeks!

h

From the Chicago Fed Website:

The Chicago Fed’s National Financial Conditions Index (NFCI) provides a comprehensive weekly update on U.S. financial conditions in money markets, debt and equity markets, and the traditional and “shadow” banking systems.

My Comments:

The NFCI updates every Wednesday morning at 8:30am Eastern Time for the week before. It is basically a measure of risk, credit, and leverage. Tightened conditions (NFCI trending higher) tend to lead to poor stock market performance and loosening conditions (NFCI trending lower) tend to lead to good stock market performance.

I have noticed that, when the NFCI changes direction from up to down, the SPY tends to increase in value until the NFCI changes direction back up again. Although technically, this would be a different entry and exit signal than the 10-200 SMA Cross, it would allow someone to phase into buys and exits of half of their position.

As an example, buy on the Wednesday open when the NFCI turns down; exit on the Wednesday open when the NFCI turns up. This entry and exit criteria is a pretty darn accurate system in itself, although sometimes you miss some bull market action.

A few good examples of exits are the Covid bear and the recent Tariff crash. Maybe Ms. Cullen could provide some further insights…..

Hey Michael – sounds interestin – let me have a look . .

Why do you use DAILY averages? You are very aware of the “noise” aspect of the market, and the WEEKLY updates would not look that different if the data were taken from weekly readings (i.e. Fridays). Although the need for “whitespace” following a crossover would still be needed, there may be less ambiguity when the cross occurs. Today’s markets move too quickly (in both directions) to use a longer timeframe, like a MONTH – the whole CoVID Bear drop scarcely took more than a month. In my limited backtesting of 10 years, the 40 week SMA and WEEKLY Price are easier to manipulate, and generate comparable results.

Hi Vern

I think that the daily data gives us the most information about what is happening in the market, each candle being the emotions of the traders on that particular day. The daily data has no gaps in it, whereas the weekly data has 17.5 hours between data points. As you know, I think that the market is simply a whole lot of people with emotions and the charts a record of that emotion. I feel I am missing out on information if I use a longer-term chart.

That being said,wekly / monthly charts are really good for seeing longer market trends – thats why I alsayw show a 5 year chart in the blogs (as well as a 3 – 6 month daily chart).

I haven’t backtested weekly or monthly data but I would feel quite twitchy using it for trading decisions.

But if you have backtested it, go for it. Everyone has different comfort levels.

h

Very insightful. Thank you very much for sharing your analysis.

Thank you Gareth!

x

h

Hi Heather,

I’ve recently been learning more about futures and I wanted to ask your perspective. Why not implement the ITM strategy using futures instead of call options?

From what I can see, futures seem to have several advantages:

No time decay.

Very deep liquidity.

Tradable nearly 24 hours a day, 5 days a week.

Low margin requirements (around 5%), which lets you keep cash in the account earning interest.

Dividends are priced in, so you effectively capture them through the futures price.

On paper this seems “too good to be true.” The main downside I can see is the risk of margin calls. But if we’re only using modest leverage (say 2x) and keeping 50% of the cash as a buffer, it would take a 50% drop in the index to trigger a margin call — and presumably the strategy would have exited long before that. And in the case of a severe market crash, both futures and ITM calls would lose money anyway, so that doesn’t seem like a unique disadvantage of futures.

Am I overlooking some important reasons why ITM calls are preferred over futures for this strategy? For example, are there tax, regulatory, or practical considerations that make options more attractive for retail investors than futures? I’d love to hear your insights.

Best regards,

Tyler Liu

Hi Tyler

the main reason is the unlimited risk – with options you have a defined risk (as in you can never lose more than you have paid for the option) And I am definitely allergic to margin calls! With options there are none, with futures there are.

Futures required margin and are marked to market daily, so you can be required to top up.

As well, options are simple, and on the same platform as stocks, and are almost as easy to trade. Futures usually require specialized accounts and have higher regulatory and capital requirements – not really suitable for non-professional traders, especially those trading retirement accounts.

Fewer brokers offer futures accounts, and require much more detailed financial disclosure, including trading experience.

So they are the practical considerations – as for tax, I am afraid I have no idea, you would need to talk to a taxation specialist.

Hope this helps

h

Heather,

1. I enjoy hearing of your travels.

2. I have been implementing your strategy but not 100% for my own travels. I recently travelled to Alaska and took half my capital out of the market. That way I could ignore the market while relaxing. I am home and will ease back in.

3. I also use Investors Business Daily, they have a scale of market exposure in 20% intervals. They are currently at 80-100% invested. I am not sure that they publish the metrics that they use to determine the ranges but they do use a running count of days of unusually large swings (making this up but something like- of the last 21 market days the number of closes with a loss of 1% or more).

4. I really appreciate your work and the willingness to share what you do. When we have been blessed, passing on what we have learned is great. I was the youngest kid of parents who were financially irresponsible, they sent my older siblings to college one sister went for years and never passed a class despite being a National Merit Scholar, majoring in partying… one sister went to college and struggling to feed herself there, sold her blood on a regular basis and dropped out but finally graduated in her 40’s. The only boy was sent to private college and my parents paid all his much more extensive expenses including room and board, no selling of blood needed. I was told “oops no money left we spent it all on your brother” thankfully I was good at math and science and got a scholarship to get a degree in Math. Saving and Investing has giving me financial security that I craved. I give talks often to civic groups and student groups about the importance of harnessing compounding in your favor and avoiding debt that compounds against you. (Including debt to go to college). Since your methods are simple and mechanical I often recommend them as taking much less time than traditional investing of hunting for the best companies. I have found it hard to let go of more traditional investing and just make the money. There is an emotional need to find those winners that is not fulfilled. I try to remind myself that the financial freedom IS THE GOAL, but I am strongly drawn to winning the intellectual game of finding outperforming stocks. For me that is the biggest deterrent to fully going to ITM

Hi a reader!

Thank you – I do understand wanting to have a holiday free of worries – and anything that lets you sleep better at night is a good thing!

I’ve just had a look at Investor’s Businss Daily – looks very busy, couldn’t see where they are currently 80% invested? $35.95 per month seems reasonable, but I don’t subscribe to websites any more (not strictly true, from time to time I am tempted, but I always reget it!)

Your experience of the money going to educate ‘the boy’ smacks of my own experience – my mother wanted me to go and work in a bank, I had to finance my own way through uni too. But it made me more resilient and inventive, so I shouldn’t complain.

Re the ’emotional need’ to find winners – I think we all have it to some extent. But every time I get the urge I look at a few of my smaller accounts here in Australia – full of ‘absolute winners’ from tips by friends ‘in the know’, and I buy in just to keep them happy (not a lot 5-10k each) Not one of them is even worth what I have paid for it!

I keep them to remind myself not to go chasing companies.

Maybe you could sequester part of your account (say 20%) to flutter on stocks and do ITM with the rest? Just a thought.

Nice to hear from you.

h

I am doing exactly as you suggest. Because of the complications of tax deferred and tax free accounts I have 13 accounts I manage for myself, husband and one of my children. I am A/B testing the ones where options are allowable are in ITM as A. The accounts where options are not allowed are the B. No clear winners in results, I am a good stock picker but getting older. I worry about mental decline, which is a huge reason to prefer your system. But will mental decline happen faster without the mental exercise… learning to speak Spanish as a hedge. Cannot recommend the app “Speak” for anyone actually trying to learn to USE another language, as opposed to STUDY a language and never be able to converse in it. No interest other than as a paid subscriber.

Investor‘s business daily is included with my Wall Street Journal subscription, they have a lot of special offers. And their current market exposure has dropped to 60 to 80%

Hi ‘a reader’ – I refuse to even consider mental decline – that can happen to someone else, not me! I’m sure it won’t happen to you either if you just refuse to entertain the possibility!

And do keep us updated about your results – always willing to learn.

x

h

Hi Heather,

Thank you for dedicating so much time to teach us. It truly is appreciated. I was thinking the same thing as Bradley. If we got out on a 5/50 cross or a 10/20 cross and then got back in when those lines crossed again instead of staying out until the next golden cross. Thanks again for all you do for us! Wishing you a wonderful week!

Hey Charity – glad it answered your question. I may have got these answers out of synch, so get back to me if I haven’t answered properly.

h

Hi Heather, thank you so much for all the effort that you put into this.

I missed out on the recent golden cross as I was working through some other financial transactions, and now I have sufficient funds to start with the ITM system. However, from the golden cross till now, the markets has risen substantially.

As pointed out in your blog earlier, there is always the chance that the market will continue to climb and climb.

What I wanted to ask is when we miss the original golden cross, is there a way to determine if it is too late to enter the ITM trade? If it is not too late, is there an alternative “out” signal rather than the death cross, so as to account for the late entry?

Thanks!

Hi Leonard,

while the golden cross is still in force (i.e. as in now where we haven’t had a death cross) then it is OK to join the bull run with the standard ITM rules.

Obviously, as you have missed out on the first part of the run your profits will not be as big as someone who got in the day after the cross, but bull runs can go on for a long time, sometimes years and you don’t want to be sitting on the sidelines missing out.

I’ve done a couple of blog posts on this in the past. Here are the links:

https://heathercullen.com/joining-the-bull-run/

https://heathercullen.com/is-it-too-late/

I hope this answers your question, if not please get back to me.

h

Thanks Heather !

This has been on my mind lately ! Thoughts of whether it’s best to protect profits on the 10/50 death cross and then get back in on the 10/50 golden cross if it bounces back up, or maybe the 10/100 crosses both out and back in if it rebounds until eventually we see a full drawdown past the 200 day in which we would fall back to the position of our original 10/200 entry . I don’t personally have the technical aptitude to figure out how to run such back tests and my feeble attempts with Chat GPT don’t seem to help. For now I’m sticking to the plan taught in the book! Having went through my first drop below 200, and sell this year, I’m hoping the pain of loss when the second time comes will be muted a bit .

Thanks again

Hi Joseph – I’ve tested and tested – always looking for the ‘magic combination’ – and it always comes out to the 10/200 cross. Which is strange, being such round numbers – I would have preferred them to be 13/197 or something unusual.

I’ve also tried getting out on a more sensitive cross (e.g. the 5/50) and then buying in when SPY reached the level we sold – but the results were not as good.

Actually, I might have another look at that and see if there’s a variation that works.

(OK showing my nerdy side)

Hopefully when we next sell signal comes we will be sitting on a nice profit which will ease the pain of any drawdown!

h

Perhaps a consideration would be scaling out with a 5/50 cross and back to full size with a 5/50 golden. This would somewhat reduce the freight of the options churn and mitigate the full-size drawdown to the 10/200 cross. Is this an easy change, or a deeper re-write for you?

HI Scott – I see what you mean- start exiting on the 5/50 cross, say 20%, then to 100% out on the 10/200. And vice versa.

Before you can backtest anything you have to have a clear definition of every possible outcome and what you will do in that eventuality.

So lets say we sole 20% on the 5/50 planning to sell another 20% on, say, the 6/70 cross, another 20% on the 7/90 cross etc to 10/200. Yes, that sounds reasonable – and might work if every 5/50 cross proceeded to a 10/200 cross.

But they don’t. Yes, every 10/200 cross is preceded by a 5/50 but not every 5/50 leads to a 10/200.

So what happens in this case? Suppose you sold 20% on the 5/50 cross but it never reached the 6/70 – when do you buy back in? And on what signal? etc etc

You have to account for the universe of possibilities – which will get very complicated!

I am not sure I have explained myself clearly, but have a look at the table in this post – and then expand it to 10 SMAs instead of 4. Instead of 8 possible orderings you would have 512!

I think my head would explode if I tried to backtest that, and I’m not sure that 100 years worth of data would be enough to test all 512 possibilities.

So – summary – it sounds like a seductive theory, but one unable to be back tested. I think. Could be wrong – let me know if I am!

h

Hi Heather,

I truly appreciate everything you do for us and if this is too much to backtest, I understand. I tried to do my own backtesting and it was just too complicated for me to follow. I apologize. But if we got out when the 10 crossed over the 20 (death cross) (or the 5 with the 50), then got back in when the 10/20 golden cross (or the 5/50) unless a true death cross happened (10/200). That is what I was wondering. Thank you again and wishing you a wonderful weekend ahead!