| Why 90% Winners Lose Money |

We’ve been looking at fashionable options strategies, and discovering their limitations:

- Covered Calls → “selling your upside”

- The Wheel → “small premiums, big risk”

- The Options Zoo → “different animals, same calls and puts”

Video

This week we’ll look at perhaps the most fashionable strategy of all: Zero Days To Expiration (0DTE) options.

What is 0DTE Trading?

Podcast

0DTE stands for “Zero Days to Expiration” and refers to options that expire on the same day they are traded. Because there is so little time remaining, their prices can change dramatically within minutes, creating both the possibility of large profits and the risk of equally large losses. Over the past few years, 0DTE trading has become one of the fastest-growing areas of the options market.

How Big Is 0DTE?

BIG. In early 2022, average daily SPX 0DTE volume was around 388,000 contracts. By 2025 it had grown to roughly 2 million contracts per day. A five-fold increase in just three years. That’s why everyone is suddenly talking about it.

Niche No Longer

What began as a niche trading strategy has become a major part of the options market. Today, almost one quarter of all U.S. option contracts traded are 0DTE options, while in the S&P 500 options market they account for around 60% of total volume. On a typical day, more than two million same-day SPX contracts change hands.

The Effect on the Market

The growth of 0DTE trading has changed the character of the market. Large volumes of same-day options create hedging activity by market makers, which can amplify short-term moves and increase intraday volatility. Markets still respond to economic news and investor sentiment, but are increasingly influenced by the mechanics of the options market itself.

Retail Traders

The popularity of 0DTE options has been driven largely by retail traders seeking leverage and fast profits. For them, the option trade is the investment. A successful day can produce returns that would take weeks or months to achieve in the underlying market.

Retail traders are estimated to account for roughly 50–60% of SPX 0DTE trading volume. Even more remarkable, more than 75% of retail traders’ SPX option trades are now in 0DTE contracts.

Are Retail Traders Successful?

In a word: NO. Retail traders lose money on 0DTE options on average. The attraction is understandable: frequent wins, enormous leverage and the possibility of making a month’s salary in a single afternoon

Why Not??

Transaction costs alone accounted for roughly 70% of retail 0DTE losses. The combination of bid-ask spreads and frequent trading creates a substantial headwind before a trader has made or lost a single dollar on market direction, however that does not seem to lessen the attraction.

Retail traders are attracted to high-volatility, lottery-like opportunities and tend to dismiss the fact that they underperform after costs.

Why 90% wins can lose money

90 winners at +$100: $9,000

10 losers at -$1,000: -$10,000

Win rate is fantastic. In reality, the account goes backwards.

Market Geniuses?

The frequent small wins create a major psychological problem: they provide powerful positive reinforcement. A trader who wins nine out of ten trades naturally begins to believe that they are uniquely skilled. Confidence grows, position sizes increase and losses are dismissed as bad luck or one-off events.

Or Poor Memory?

The mind remembers the many successful trades and tends to discount the occasional disaster. A strategy can make a trader feel like a genius for months, while quietly losing money in the background.

A Book! A Course! An Influencer!

And, of course, during the ‘genius’ months they write a book, launch a course or start a YouTube channel explaining their secret formula for success, attracting even more traders to the strategy.

What Does This Mean For ITM?

Fortunately, this has little impact on the ITM strategy. ITM positions are typically held for months not hours and are designed to capture major market trends rather than short-term fluctuations. While 0DTE trading may create noise from one day to the next, ITM is focused on the tide, not the waves.

What Really Matters . . .

The lesson extends beyond 0DTE. A high win rate is not the same thing as a profitable strategy.

It’s not how often you win, but how much you make when you’re right and how much you lose when you’re wrong.

To the Markets . . ..

A short week, and coincidentally it follows the June quarterly options expiration.

Roughly 28% of all listed options open interest rolled off, making it one of the largest expiration events on record. More than $8 trillion of options exposure expired, highlighting just how important the options market has become.

The June expiration was not large because traders suddenly became more active. It was large because options have become one of the dominant ways investors express views, hedge risk and speculate. The sheer size of the expiration shows how important the options market has become to the functioning of the broader stock market.

SPY Charts

SPY has been consolidating most of this month, and volumes have returned to normal.

Longer term it is still above the established trading channel. Probably time I redrew that as it is past its use-by date.

SPYG Charts

SPYG also in a consolidation phase. You may be tempted to ‘see’ a ‘head and shoulders’ pattern. Personally, I’ve never thought that pattern worth noticing as it relies too much on the person drawing it (subjectivity) but I’ll probably now be proven wrong!

Long term it is sitting snugly in the trading channel.

QQQ Charts

Looks as though it is heading back to its previous highs:

Longer term it is sitting above the trading channel. Probably needs to be redrawn also.

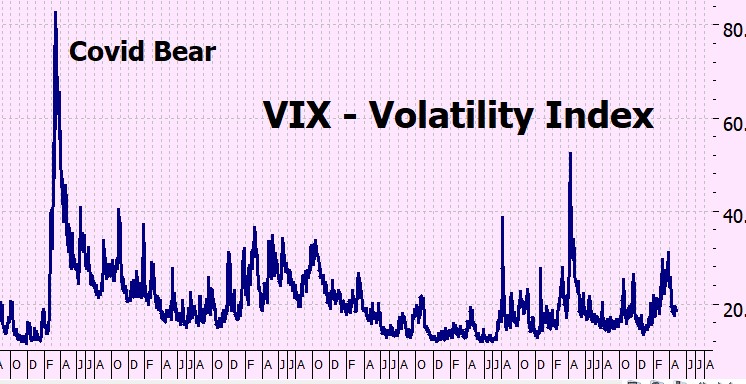

VIX Chart (Volatility)

VIX still in low-volatility territory.

ITMeter

The week ahead . . .

Monday

- S&P Global Flash Manufacturing and Services PMI data

- Markets continue to digest last week’s quarterly options expiration and positioning changes

Tuesday

- Richmond Fed Manufacturing Index

- Earnings: Carnival (CCL), FedEx (FDX)

Wednesday

- New Home Sales

- Earnings: Micron Technology (MU), Paychex (PAYX)

Thursday

- Durable Goods Orders

- Final Q1 GDP revision

- Personal Income and Spending

- PCE Inflation (the Federal Reserve’s preferred inflation measure)

- Earnings: Darden Restaurants (DRI), McCormick (MKC)

Friday

- University of Michigan Consumer Sentiment

- Wholesale Inventories

The key event this week is Thursday’s PCE inflation report. Inflation remains the market’s primary concern and any surprise could influence expectations for future interest-rate decisions. Investors will also be watching Micron’s earnings for clues about continued demand in the AI and semiconductor sectors.

The futures . .

Looking rather dismal, but a lot more cheerful than 2 hours ago . . . .

Thank you . . .

. . for the lovely get well wishes – they are truly appreciated. I’m day 12 after the surgery, still on crutches and can’t drive for another 4 weeks 4 days – but things are looking up. And while recuperating I can watch this every night from my new place:

Heather

Trade the tide, not the waves

Q & A

I am sure that I have missed some questions while I have been out of action – so if you would repost them here I’ll get right onto them.

14 Responses

I was going to send a picture, but instead I’ll describe it.

In the ThinkOrSwim Trade tab and Option Chain section, there is a field called Strikes (between the CALLS and PUTS section] which drops down and allows the selection of the number of strikes to include around the ATM price. You can type your own selection or select from 4, 6, 8, 10, 12, 14, or ALL.

Glad you’re back! Going to look into self-driving EV’s?

Hey Rick – no, I enjoy driving my little MX5 (manual) too much!

h

Glad you’re healing well and enjoying the ocean view.

HI Stephen – yes, totally loving it. today is perfect – no breeze, blue sky, calm ocean – absolutely lovely!

h

Heather, you never cease to amaze me in all you do for us!

HI Andrew – thank you! It is comments like this that keep me going!

h

Schwab shows DITM call option strike prices for SPY only for the 2026-Dec-12 expiration date. For other expiration dates between 6 and 12 months from now, the lowest call option strike prices are around $737. Supposedly, the exchanges remove the DITM strike prices because those options are rarely traded — except that _we_ want them for ITM! Am I doing something wrong? I hope that the availability of the DITM options doesn’t make it harder to execute the ITM strategy.

Wilson

Hi Wilson,

I’m looking at the SPY option chain on Schwab right now and I can see DITM call strikes starting at $150 for December 2026 and $50 for January 2027 – about as deep in-the-money as you could want.

I have never heard of exchanges removing DITM strikes because they are rarely traded, so I’m not sure where that information came from.

My suspicion is that you may have inadvertently applied a filter to the option chain. Try setting custom strikes (for example, 300–400) and custom expirations (for example, Dec 18, 2026 to Jan 15, 2027) and see if the missing strikes reappear.

I have never had any difficulty obtaining suitable DITM options for the ITM strategy. If you’re still having trouble seeing them, please let me know exactly which platform you’re using (Schwab website, Thinkorswim desktop, mobile app, etc.) and I’ll see if I can help further.

Heather

I see all of the strikes on the Trade Ticket page now. I had been looking on the Options Chains page, which didn’t show all of the strikes. Thanks, Heather.

Hang in there. I know that it can get difficult to stay off your feet, even when it is needed. Keep the long viewings mind, you are good at that!

Thank you!h

Re the win loss record versus whether a strategy is a winner or loser, my favorite link to point at (and which lives in every spreadsheet tracking a strategy I’m studying or using) is:

https://en.wikipedia.org/wiki/Kelly_criterion

The Kelly criterion is actually conservative at least in the sense it expects your losing bets will lose 100% and your winning bets will lose the proportion B. You can read through the Wikipedia article to “investment formula” if you have statistics that show you lose less than 100% when you lose.

Your mileage may vary, no guarantees here. But it’s of interest for sure.

Hey Bob,

I read the Wikipedia explanation and, about halfway through, I lost the will to live!

Seriously though, Kelly is all about position sizing, and the mathematics is quite elegant. The problem is that it requires you to know two things:

1. The probability of winning.

2. The size of wins relative to losses.

In the real world we don’t know either of those with any certainty. We can estimate them from historical data, but they are still estimates. Small errors in those assumptions can produce very different Kelly recommendations.

So while the mathematics is impressive, I’m less convinced by the foundation it’s built on. As the saying goes: garbage in, garbage out.

h